In this episode of the podcast, Tomasz Szpyt speaks with Łukasz Jachna, a member of the management board and Chief Capital Markets Officer at 7R, about the various types of warehouse facilities and their appeal to…

In this episode of the podcast, Tomasz Szpyt speaks with Łukasz Jachna, a member of the management board and Chief Capital Markets Officer at 7R, about the various types of warehouse facilities and their appeal to investors.

In this podcast, you’ll learn, among other things:

– How do multi-tenant, industrial, BTS, City Flex, and SBU warehouses differ from one another?

– Which properties are attracting the most interest from investors?

– How do a building’s profitability and investment risk vary depending on the type of building?

– What kind of investors does 7R work with?

Tomasz Szpyt: Good morning, my name is Tomasz Szpyt, and welcome to the 7R.Blog.On podcast series. Together with our guest experts, we’ll be discussing current trends in the warehouse real estate sector. Joining me in the studio today is Łukasz Jachna, a member of the management board and Chief Capital Markets Officer at 7R. Good morning, Łukasz.

Łukasz Jachna: Good morning, hello.

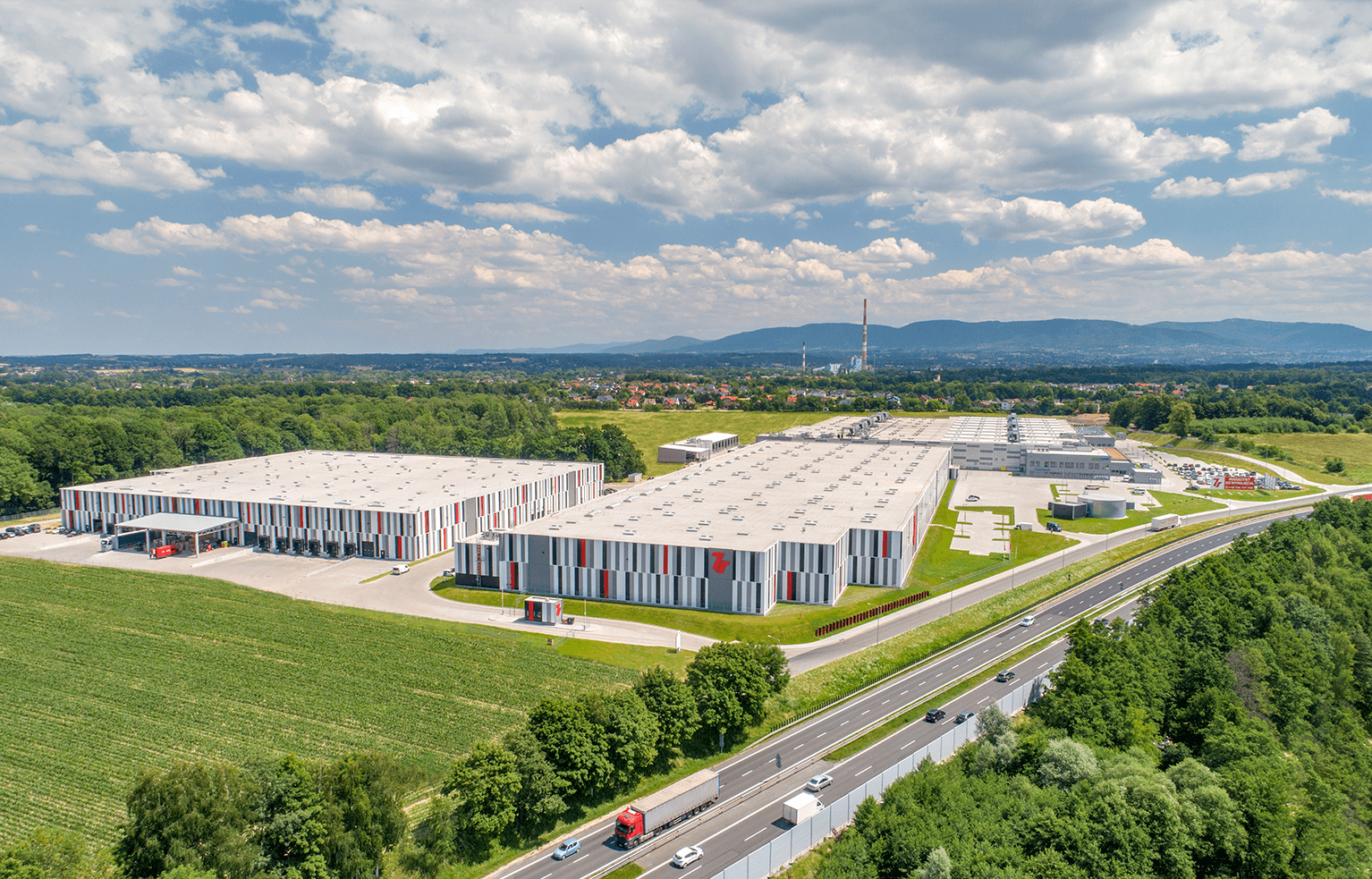

Tomasz: Today we’re going to talk about warehouses—about whether they’re really just simple real estate, or if a warehouse actually has at least a few different facets. What could possibly be complicated about a warehouse? Just ordinary boxes, shelves, forklifts, loading docks… Someone might say that, but is it really such a simple facility? There are probably as many types of warehouses as there are functions tenants want to accommodate within them. For example, we have multi-tenant facilities, production facilities, BTSs, City Flexes, and even data centers. The investment appeal of a facility also varies depending on its type. And here, Łukasz, a question for you: What are the differences?

Łukasz: Yes , great. Thank you for mentioning all these types of warehouses we’re discussing. It’s actually not as simple as it seems at first glance. Of course, compared to other asset classes, warehouses seem the easiest in terms of the actual construction process, and they look very straightforward at first glance. However, the real challenge lies in the details, as always. The warehouse types mentioned differ primarily in their operational nature for the tenant. Among other things, the most important factor is the utilization of the space we can fill with the tenant. As a warehouse developer, we always strive to meet the challenging and highly complex operational needs of our tenants, because we know this is a critical aspect of their business operations.

That is why 7R has its own team of architects and designers, which allows us to create truly bespoke products. At the same time, we strive to structure these projects so that they represent a highly attractive investment opportunity for international institutional investors,

says Łukasz Jachna

Chief Capital Markets Officer, Member of the Management Board at 7R

This is important because, starting with multi-tenant warehouses, I’ll briefly outline how it works. This is a multi-tenant warehouse, meaning it’s designed to accommodate several tenants in a single location. Since a single tenant in a given location doesn’t require such large spaces, we, as the developer, strive to build a highly diversified park where all these tenants can be accommodated. We’re generally talking about 5–7 tenants per park, with a size of 50,000–100,000 m². Many investors are interested in this type of product because, in reality, they are buying exposure to the economy and specific industries. At the same time, they are also buying diversification in the sense that if, for some reason, one of the tenants were to change its strategy, leave, or go bankrupt, they would still be able to ensure specific returns for their end investors. On the other hand, it is also interesting because today, in the multi-let warehouse market, five-year leases are the standard. This provides great flexibility for both tenants and investors, because for five years—that is, the specific period during which both the tenant and the property owner agree to certain terms regarding price and space provision— but at the same time, it is also important because after these five years, there is a so-called “deal letting,” which is a discussion with the tenant regarding the extension of a given space, or a change in the so-called tenant mix—that is, the tenants we have in a given park. Many investors see great potential in this, as it gives them a unique approach when it comes to the strategies they can employ. They can monitor how individual tenants are growing, perhaps offer them more space as part of the expansion of their core business, or have more options when it comes to selecting those specific tenants, or propose a much longer-term lease to someone if they see that potential. This versatility of multi-let warehouses is particularly interesting because there are specialized funds that, in fact, exclusively accumulate this type of investment product. At the same time, they view other warehouse types—which we’ll move on to next—such as industrial and BTS, with much less interest. The abbreviation BTS stands for build-to-suit…

Tomasz: So, custom-built warehouses?

Łukasz: Exactly, custom-built warehouses, but also custom-built warehouses in the context of very specific solutions. In such cases, we say that there is only one tenant in a single building because that’s what their operations require—critical access control or a complex production process—hence the name BTS. This is important because there is much greater involvement here when it comes to the tenant’s entire core business process. This is because the tenant often doesn’t know exactly what kind of warehouse they need. They have specific technology—such as manufacturing, packaging for e-commerce, and similar solutions. That is why it is very important to look at this not only from the real estate perspective, but also from the perspective of the tenant’s operational process itself. Our employees from both the leasing and technical departments assess which solutions are suitable and how to organize the production cycle within a given layout—that is, the space available to a tenant within the building—so that it works for them. At the same time, at 7R, we think much more long-term and strive to make these custom-built warehouses much more versatile. On the one hand, custom-built warehouses involve a longer lease agreement—we’re usually talking about a lease signed with the tenant for at least 10–15 years—but of course, this is a period agreed upon with the tenant. After this period, a discussion arises as to whether the tenant will decide to extend the lease agreement or whether their business operations no longer fit the given type of building and they wish to change the space. So even though we’re talking about custom-built warehouses, at 7R we try to tailor them to the operations of a given BTS tenant so that, if necessary, they can be converted at a relatively low cost into the type of multi-let warehouse I mentioned earlier. This is important because our investors who purchase BTS projects on the one hand, are essentially buying the long-term benefits of the lease agreement—that is, the cash flow generated by the lease—but on the other hand, they also want some alternative, because by definition, BTS buildings are typically in less obvious locations, as they are closer to our tenants’ production sites or their core operations. Thus, at first glance, these are not super obvious locations. Of course, as part of our collaboration with these tenants, we try to encourage them to be closer to transportation routes in Poland, to be closer to the 7R hubs that we are creating in both highly developed and developing markets. In most cases, this is possible. Sometimes, for technological reasons, this isn’t possible for the tenant, so the tenant simply chooses a specific location, which we agree to, and we carry out the project together. This is a holistic approach at 7R, where on the one hand we meet our tenant’s expectations, but on the other hand we think not only as a developer but also through the eyes of an institutional investor.

That is why 7R projects are highly sought after in the investment market, because it is the very essence of this so-called “alternative use”—that is, future functionality, not just today’s—that offers our investors many more potential investment strategies. This is a highly desirable feature,

adds Łukasz Jachna

Tomasz: Exactly , Łukasz. You mentioned that 7R’s properties are in high demand in the investment market. Why don’t we move on to the City Flex category? Not long ago, 7R closed a fairly large deal involving the sale of several such properties. Could you explain, on the one hand, how this type of warehouse differs from, say, a big box facility, and share a few more words or sentences about the transaction itself?

Łukasz: Jasne, jak najbardziej. Przede wszystkim magazyny typu last mile, czyli tzw. ostatniej mili, również inaczej nazywane SBU, czyli Small Business Units. W naszej firmie mamy własną kategorię, która nazywa się 7R City Flex, czyli magazyny ostatniej mili. To jest nasz autorski branding, niewytworzony przypadkowo, ponieważ jako pierwszy deweloper w Polsce postanowiliśmy skupić się na zbudowaniu całego programu City Flexów, czyli magazynów ostatniej mili, w głównych miastach w Polsce. Widzimy z tego tytułu bardzo duże korzyści, ponieważ, tak jak dobrze zauważyłeś, jest to totalnie inny produkt. Po pierwsze lokalizacja takiego magazynu jest w ramach aglomeracji. Po drugie bardzo stawiamy na transport publiczny. Po trzecie są to magazyny troszeczkę mniejsze niż tzw. big boxy, ponieważ mówimy tutaj o wielkości typowego magazynu city flexowego od 10 do 15, maksymalnie do 20 tys. m2. Jednocześnie są przygotowane pod dużo mniejszego najemcę. Jest to najemca, który nie potrzebuje wynająć 50-100 tys. m2; to jest najemca, który potrzebuje wynająć 1-2 tys. – to po pierwsze. Po drugie udział biur w takim magazynie jest dużo większy, ponieważ jest tam więcej pracowników biurowych niż tylko magazynowych. Wynika to z faktu, że często naszymi klientami są albo showroomy, e-commersowi najemcy, tudzież operacje tzw. pick-up location dla wielu graczy, chociażby DIY w postaci Euro RTV AGD, który powierzył nam budowę części swojej sieci logistycznej pod kątem przyjmowania zwrotów i odbiorów produktów przez klientów prywatnych. Jest to o tyle ciekawe, że wymagamy dużo większego przemyślenia powierzchni w City Flexie, ponieważ chcemy, żeby te projekty były maksymalnie uniwersalne, żeby ten unit, czyli potencjalna dedykowana powierzchnia pod jednego najemcę, był w miarę wygodny pod różne typy operacji. Jednocześnie tak jak mieliśmy przy okazji multi-let i big boxów, chcemy też myśleć tak, jak przyszły inwestor, więc te podziały muszą być dużo bardziej uniwersalne w przyszłości, ponieważ tak naprawdę rozmawiamy dzisiaj z najemcami, których potencjał wzrostu jest największy. Oni dzisiaj zaczynają od 1-1,5 tys. m2, ale w ramach rozwoju ich core biznesu zakładamy, że będą się rozwijali, jak chociażby super rosnący rynek e-commerce w Polsce, więc za X czasu będą potrzebowali większą powierzchnię. Tutaj też mówimy o umowach na okres średnio pięć lat. Oczywiście są jakieś wyjątki pod kątem specyfiki konkretnego najemcy, ale generalnie też takim typowym okresem to jest pięć lat. Te magazyny są bardzo pożądane przez inwestorów, ponieważ po pierwsze to jest bardzo rozpowszechniony typ produktu u naszych zachodnich sąsiadów, w Polsce dopiero raczkuje. Były wcześniej realizacje przez różnych deweloperów w poszczególnych miastach, ale my jako 7R zrobiliśmy program, który jak wspomniałeś przed chwilą, udało nam się uplasować z Macquarie Group – to jest duży fundusz inwestycyjny specjalizujący się w infrastrukturze i nieruchomościach globalnie i tak naprawdę nasza współpraca trwa już od kilkunastu miesięcy. W listopadzie 2021 zakonczyła się realizacją kolejnego projektu. Obecnie w ramach tego portfela mamy już 80 tys. To jest istotna wielkość portfela, jeżeli chodzi o magazyny ostatniej mili. Pracujemy nad kolejnymi lokalizacjami, widzimy, że ta współpraca odbywa się bardzo przejrzyście, ponieważ zarówno oczekiwania inwestora, jak i 7R są zbieżne, bo mówimy o absolutnie core’owych lokalizacjach, mówimy tutaj o najwyższej jakości, jaką można zaoferować najemcom i mówimy tutaj o spełnieniu wszystkich wymogów ESG w postaci paneli fotowoltaicznych, ładowarek do samochodów elektrycznych, automatycznej kontroli dostępów i wszystkich udogodnień dla najemców, które możemy na danej lokalizacji zaprezentować, ale tak naprawdę to najbardziej holistycznym podejściem jest możliwość zaoferowania naszym najemcom i pracownikom transportu publicznego do tych lokalizacji – coś, co nie jest możliwe przy okazji big boxów, ponieważ są przeważnie zlokalizowane dużo dalej od centrum miast. Ta unikatowość powoduje, że jest to bardzo unikatowy produkt, z którego się bardzo cieszymy, bardzo go rozwijamy, wymaga to bardzo dużo pracy naszego teamu, ponieważ mówimy też o najemcach, którzy często dopiero rozpoczynają swoją przygodę z najmem instytucjonalnym, więc pojawia się tam jakiś aspekt edukacyjny. Ale przy odpowiednim podejściu do klienta, przy odpowiednim pokazaniu mu wszystkich zalet tego typu umowy, w bardzo krótkim czasie rozumieją, że jest to świetne rozwiązanie dla nich. A my cieszymy się, że tak naprawdę magazyny ostatniej mili w wykonaniu 7R, to jest znalezienie najemców na praktycznie 100% dostępnej powierzchni jeszcze przed zakończeniem budowy, co najlepiej odzwierciedla, jak bardzo projekty tego typu są potrzebne w Polsce, jak i również jak bardzo najemcy ufają w naszą jakość, egzekucyjność wykonania super projektów.

Tomasz: Exactly, the property is top-notch, the tenant is top-notch, the investor is top-notch… How do the profitability and risk of this type of investment vary depending on the type of warehouse—or, more broadly, the type of storage facility?

We’re talking about the current climate, where warehouse projects are in high demand because many institutional investors have realized that this is no longer just an ugly big-box facility on the outskirts of town that no one pays attention to, but rather a key segment not only of the real estate market but of the entire economy. This is because a strong economy in a given country directly translates into increased international trade and warehousing, not to mention the shock caused by Covid last year. This is interesting in that, on the one hand, we are now seeing a very large influx of capital into this asset class, while on the other hand, despite the huge supply currently on the market and even greater demand, there is still a shortage of high-quality products—as you so aptly put it—that are top-notch. Hence, investors are willing to pay a certain premium for owning top-tier assets.

adds Łukasz Jachna

When it comes to distinguishing between our different types of warehouses, the key factor is precisely the risk you mentioned, which is actually tied to the length of the lease agreement. Apart from location and product type, the reality today is that investors—and this is not a uniform approach, as there are some institutional investors who believe that greater value lies in having a single tenant in the aforementioned BTS for 15–20 years, whose covenants, i.e., credit rating, financial statements they can verify today, they can check the industry in which the tenant operates, and have “peace of mind”—meaning they’re buying the tenant’s cash flow over 15–20 years and are willing to pay a certain premium for that. This is interesting in that the premium for this tenant is relatively high, but on the other side of the scale, we have investors who believe that, paradoxically, the diversification I mentioned earlier regarding big boxes is much more appealing, because they aren’t investing their money in a building with only one tenant, and in the event of a situation they can’t control today, they would lose all their cash flow. They prefer to have this diversification in the form of several tenants and are not afraid of this active commercialization after the base lease period—that is, those approximately five years—so this is something they value highly. On the other hand, there are small last-mile warehouses, which, on the one hand, share similar characteristics with big boxes but are located closer to cities, which automatically means that the land price itself is much higher than in the case of a big box. This gives rise to an additional scenario among these investors in the form of so-called “alternative views,” meaning they are considering and speculating on whether the location where City Flex is currently built will look the same over the long term. We’re not talking about five years here; it’s more like 10–15 years. But from their perspective, this represents added value in the form of paying a premium for this type of product because they have an additional strategy in mind. Perhaps in 15–20 years, this location won’t be just a warehouse; perhaps it will be office space, residential… time will tell. Additionally, this specific aspect of having an even greater number of smaller tenants—for example, through a program—is interesting in that, in reality, an investor purchasing last-mile projects is betting on a very significant increase in their tenants’ potential; that is, they see that they are investing in the most dynamic sector of the economy and accept the fact that they have much greater so-called active asset management, meaning the management not only of the building itself but also of the tenants within that building in the context of retaining them within the purchased last-mile portfolio.

Tomasz: Exactly—what are the risks associated with the types of production facilities we haven’t mentioned yet? How do investors view this kind of investment?

Łukasz: For us, production projects are essentially BTS projects, but very specific ones where we’re unable to apply our holistic approach—that is, to fit a BTS project within the standard framework of a multi-year building. In such cases, first of all, we’re talking about a lease term of at least 15 years—that’s the absolute minimum, though 20 years is generally recommended. This results in a very specific building that’s essentially tailored exclusively to a particular type of tenant, and here the tenant’s financial capacity plays the most significant role, as it’s the key factor. It is considered the most important factor when an investor selects this type of product. For us, this is interesting in that we see that, thanks to this, our organization can better understand the needs of our tenants, because a potential tenant comes to us with such a specific business process that the educational process within our company itself is already interesting, and additionally, it’s something that is incredibly sought after today by very passive investment funds, which don’t really consider alternative views or location—they look solely at covenants and cash flow. They are interested in the very long-term horizon that such a production facility can provide. On the one hand, these are highly sought-after projects; on the other hand, they represent a distinct category within the broader context of logistics and the industrial market in Poland. We view this more as a way to build additional expertise, but also to show our potential and current tenants that nothing is truly impossible for 7R; we are able to meet every need and find solutions that enable our tenants’ operations.

Tomasz: Thank you , Łukasz. The warehouse market has received a real boost in recent years. This growth is ongoing and very dynamic, and it looks like it will continue for at least a few more years. I wish you continued success in the commercialization and sale of warehouses. Thank you very much for the conversation, and thank you all for listening to the podcast from the 7R.blog.on series. See you in the next episode.

About the author

Author's Bio

Lilianna (Elżbieta) Laudy

Marketing & Digital Manager

Lilianna Laudy serves as Digital & Marketing Manager at 7R SA, where she is responsible for developing digital and marketing initiatives that support brand visibility and online communication…